2019 has had its challenges – What will 2020 bring?

Posted date: December 12th 2019 . Author Gregory Preston .

On the geopolitical front, Greg Preston commented that the 2019 British election result on December 12 has seen a resounding mandate to the Tory Party and Boris Johnson to finally bring some sense to Brexit into 2020.

This together with the likelihood of a resolution to the US/China trade wars and the refreshed North America Free Trade Agreement are good for economic prospects into 2020. The impact of these geopolitical events on global capital markets during 2019 in terms of volatility, risk and uncertainty had been profound.

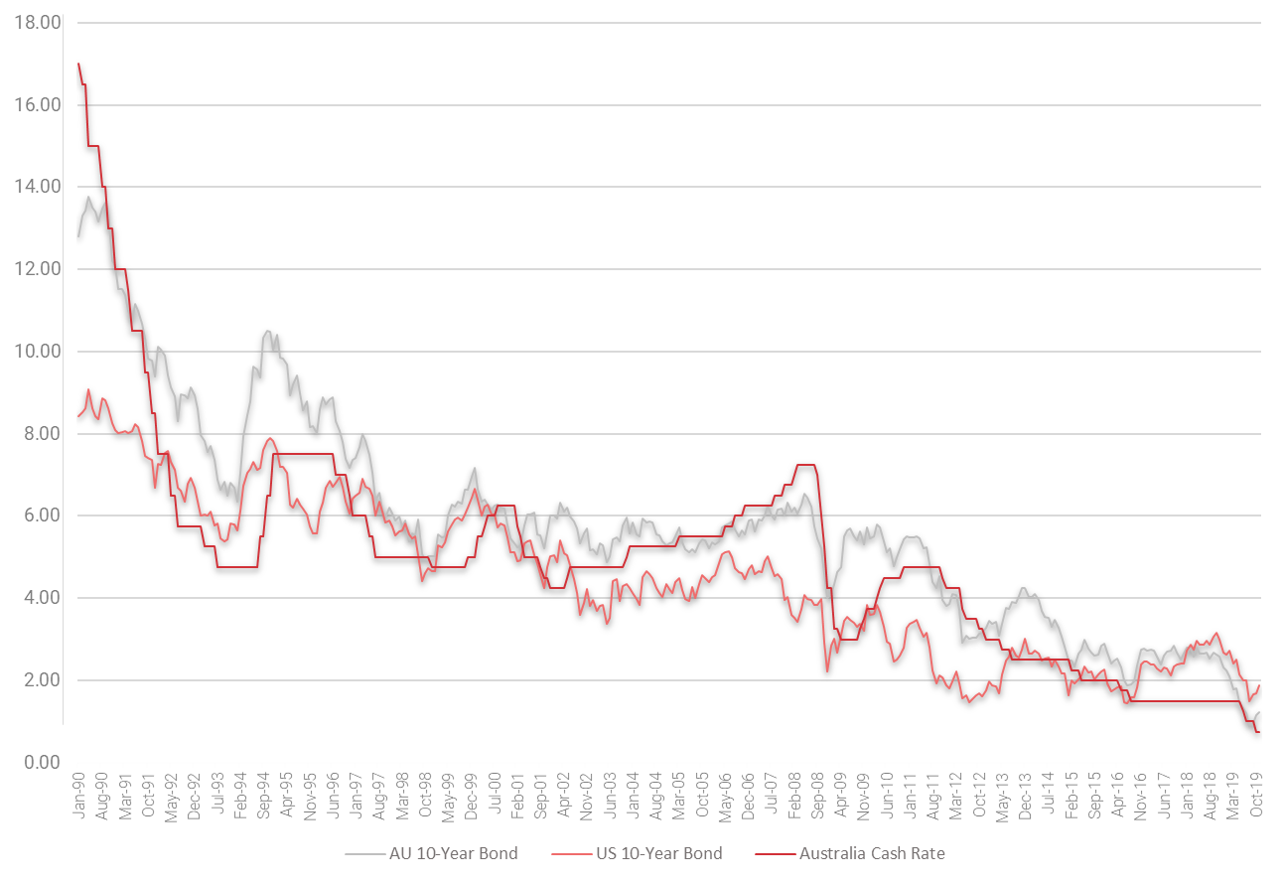

Global bond yields and the quantum of bond values trading at negative yields ($17 Trillion US as at September 2019) has and continues to be perplexing. More so is the reduction in rates for bond markets generally as well as the compression flow-on effect to discount rate and yields.

Where the risk-free long-term bond yield is implicit as a starting point in determining the cost of equity in models such as the Capital Asset Pricing Model (CAPM), market risk premiums are being looked at very closely as we come to grips with the continuing impact of lower rates. The same also goes to the cost of debt side of the capital stack equation. The cost of debt has also lowered where bank bill swap rates have reduced, and debt margins have evolved.

The result of lower costs of both debt and equity and the lowering of the cost of capital (i.e. reduction in a firm’s Weighted Average Cost of Capital – WACC) has seen further reductions in discount rates and multipliers for firms buying and selling all asset classes.

In an investment real estate market application of this logic, the lowering of cost of capital of the REIT’s has seen compression in discount rates during 2019 with further compression anticipated in the December round of Australian REIT valuations.

There is also a direct compression relationship of this logic to capitalisation rates and ultimately initial yields that fall out of sale transactions. For example, at the start 2019, the Australian 10 Year Bond Yield stood at approximately 2.27% and at the date of writing, on 5 December 2019, it stood at approximately 1.095%.

Source: Reserve Bank Australia

Coming to grips with the income multiplier effect of discount rate and cap rate compression in the context of increased asset valuations can be a challenge when compared to historic multipliers.

Given rate movements since June 2019, we are anticipating further yield compression in the December 2019 round of REIT valuations for long WALE commercial and industrial assets. Retail assets may benefit from yield compression where cash flows are not impaired based on the current challenging nature of retailing at a tenant level.

Australian residential real estate values have behaved somewhat like a roller coaster in 2019. At the commencement of the year residential markets continued to order tramadol online cod be in decline and there was a distinct threat that the Labor party’s pre-election tax policies could exacerbate market decline if they were successful. Post the Liberal/ National Party election win, and moving forward from the Banking Royal Commission, the year’s end has seen a return to confidence and residential market activity with growth in Sydney and Melbourne’s residential markets anticipated in 2020. This has also been unpinned by the growth in the Non-Bank lending sector and the improved availability of credit.

Sydney’s real estate markets continue to be buoyed by the roll-out of infrastructure, however this presents some challenges to existing landowners where their lands are to be acquired for many and varied public purposes.